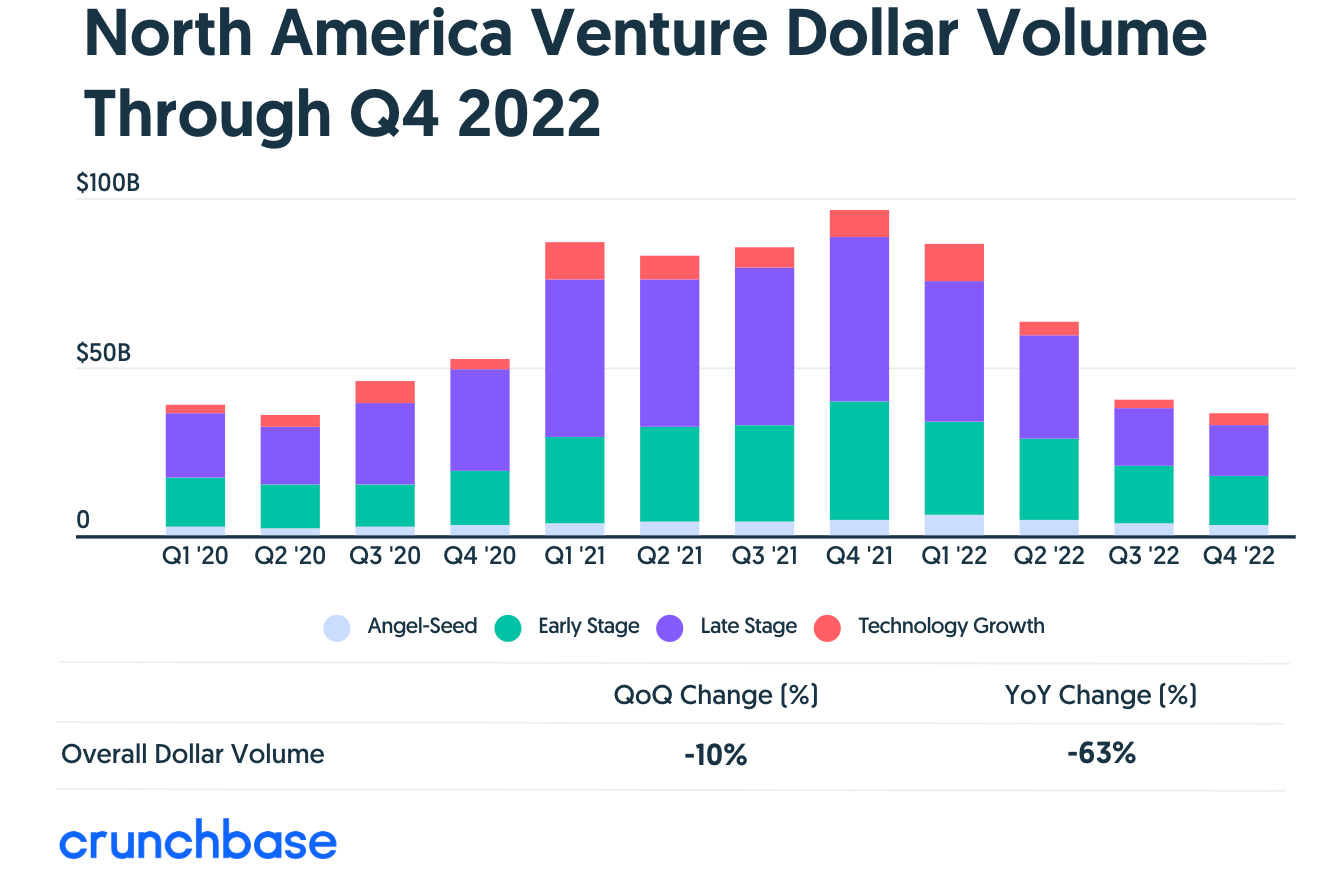

During the last few years low interest rates and money printing led to a funding bubble in private technology. Many startups received pre-emptive extra “free rounds” and hired teams much larger then their stage or progress merited. In parallel, abundant money and secondaries meant companies that should have shut down or sold kept going (indeed – this was a pre-COVID phenomenon from ~2017 or 2018 on). There was always another round or extension to keep companies without real product-market fit going. Or founders sold secondary stock in multiple rounds instead of selling a company that wasn’t really working.

These trends have resulted in an overhang of companies that either (1) lived without product market fit and survived well past their natural expiration point, or (2) hired way ahead of progress and burned large sums with high valuations and now are stuck with little progress per dollar and a large preference stack.

When will companies run out of cash?

Many companies are likely about to meet a hard reckoning. This is likely to start end of 2023 and accelerate through end of 2024 or so. The likely timing is +/- 6 months. It is based on when companies last fundraised at scale, 2021, and how much runway they raised.

Many companies raised 2-4 years of runway in 2021 (and Q1 22). A company needs to fundraise when it still has 9-12 months of cash left.

For example, below is the cash out dates for companies assuming they raised 2.5 years of cash in 2021. As you can see, in this scenario many companies of this type cash out by Q3 2024.

For 3 years of cash, cash out largely happens by end of 2024.

Adding an extra year of cash (4 years cashed raise) obviously just pushes things out an extra year – so we should expect a tail of companies that raised even more in 2021 to run out of money in 2025. For a CEO not making much progress, it might not be worth waiting that long to make a radical change to one’s business.

There is likely a mix of companies who have raised anywhere from 2-4 years of cash in 2021 that will not grow into prior valuations, and will need to find an exit or shut down. As such Q3 2023 through end of 2024 (and maybe part of 2025) seems roughly when these companies will start to seek exits and or shut down.

There will also be a set of companies that raised a very large amount of money, will cut burn via multiple layoffs, and roughly have infinite runway without much revenue growth. More on these companies below.

The ongoing correction in mid-to-late stage tech is increasingly decoupled from macro

The ride up, and the cracking point, of tech valuation inflation were driven in part by the macro environment of low interest rates and money printing (and probably in part due to the collective mass fever dream of people stuck at home during COVID). Private tech and market macro (inflation, interest rates) are now decoupling in most ways that will matter for the next 18 months for pre-existing mid-to-late stage companies.

Low interest rates plus money printing puffed up public and private market valuations leading to over funding and over hiring.

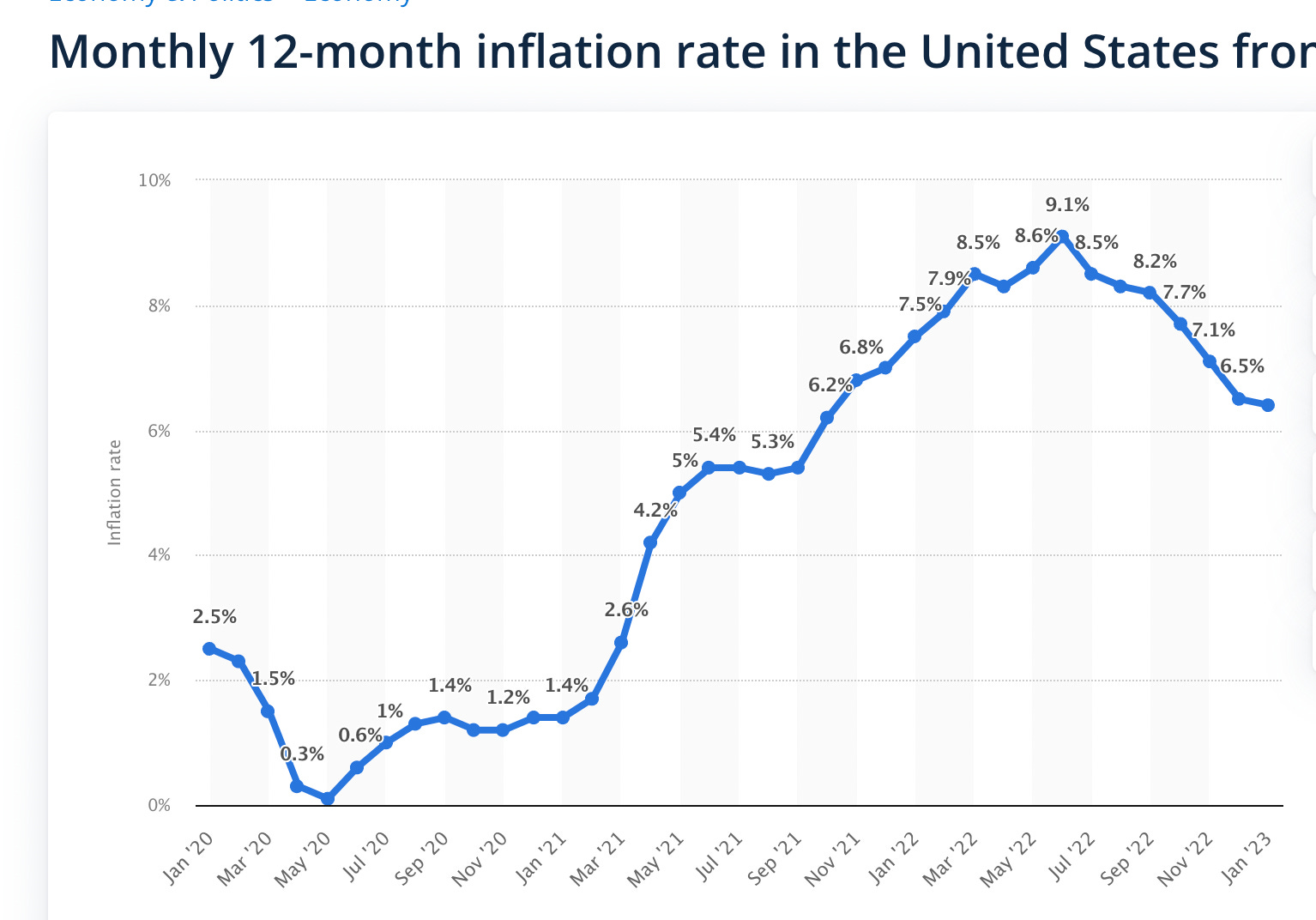

This also led to inflation.

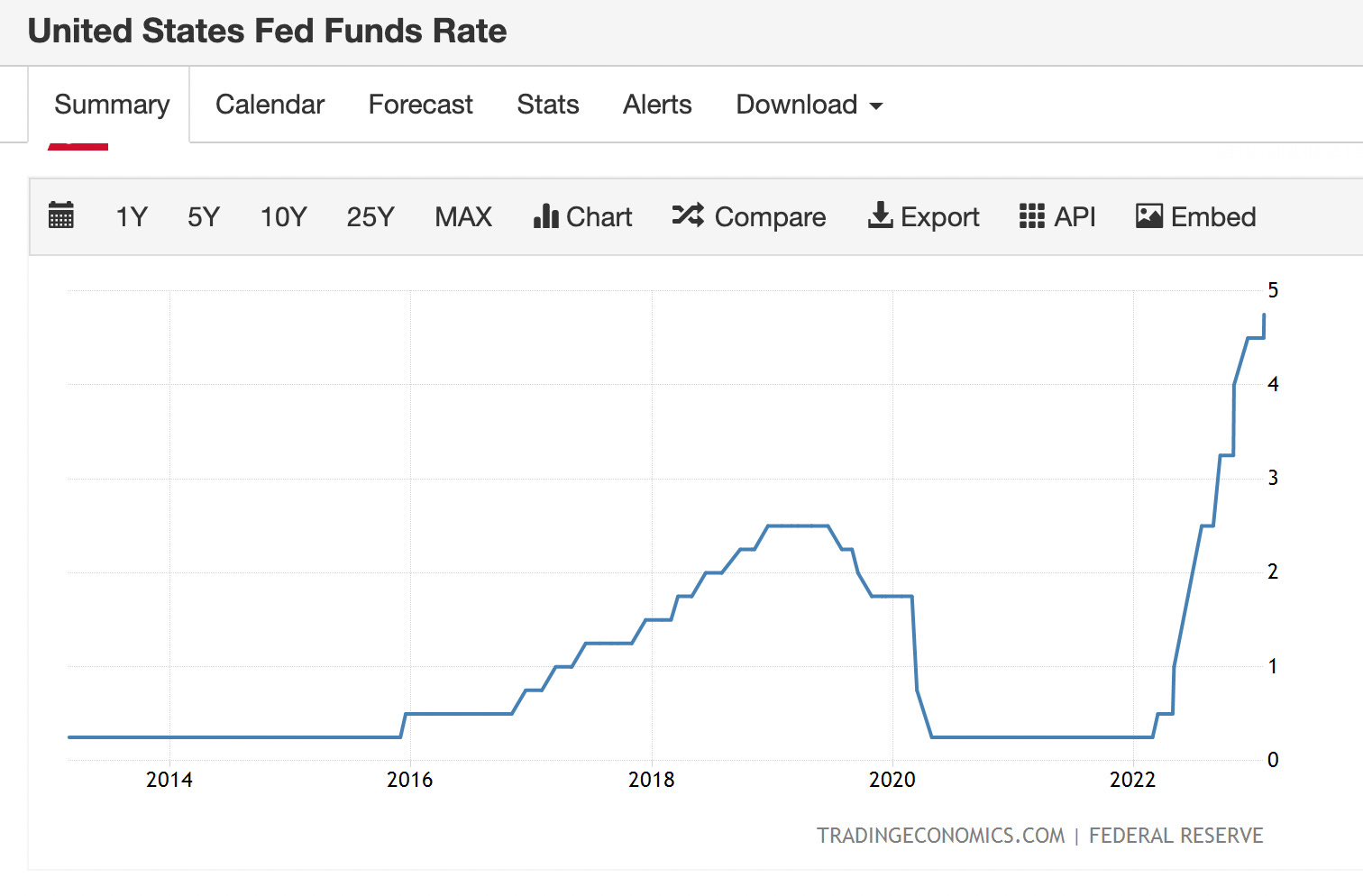

In response to inflation, interest rates were hiked.

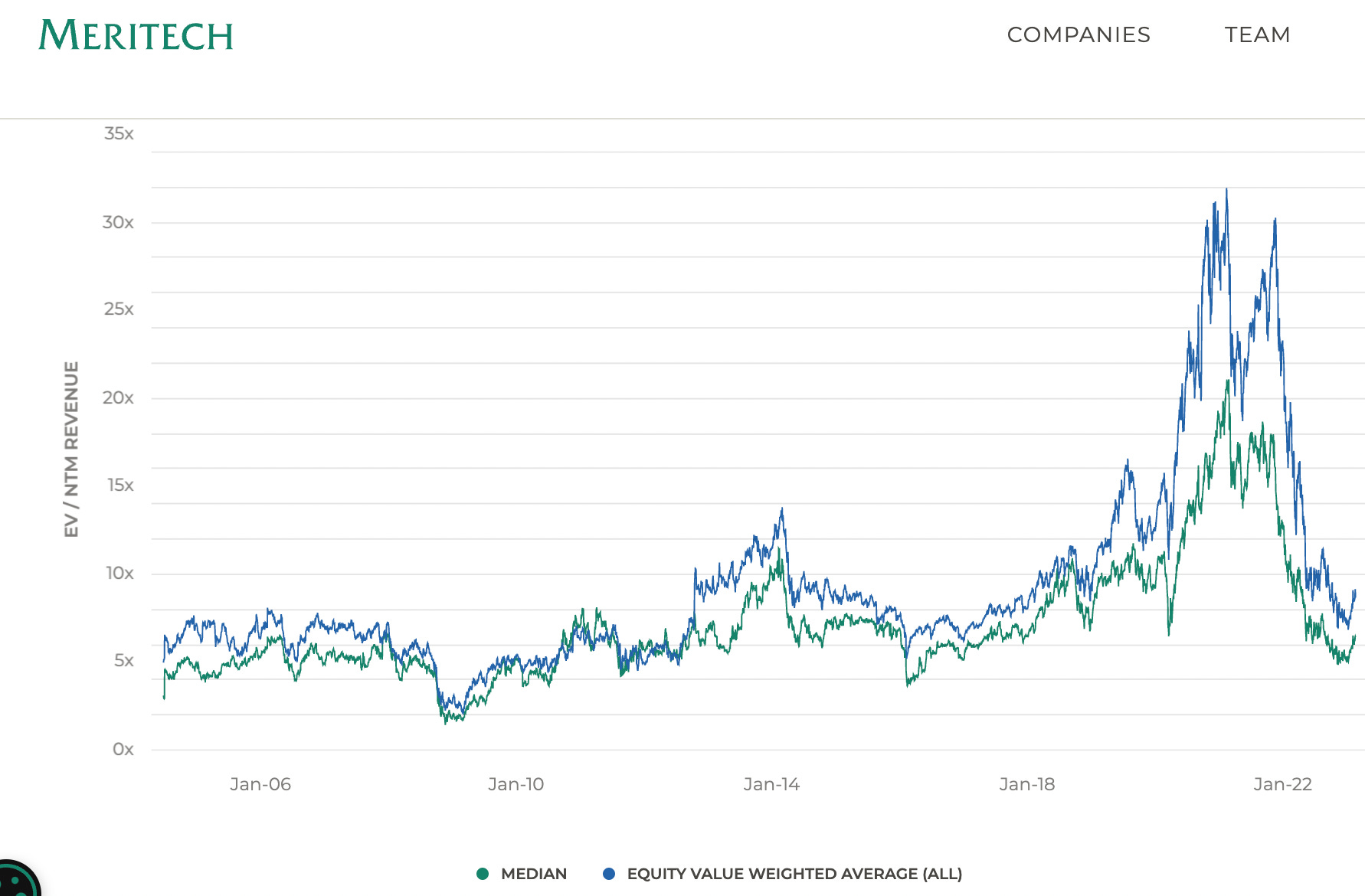

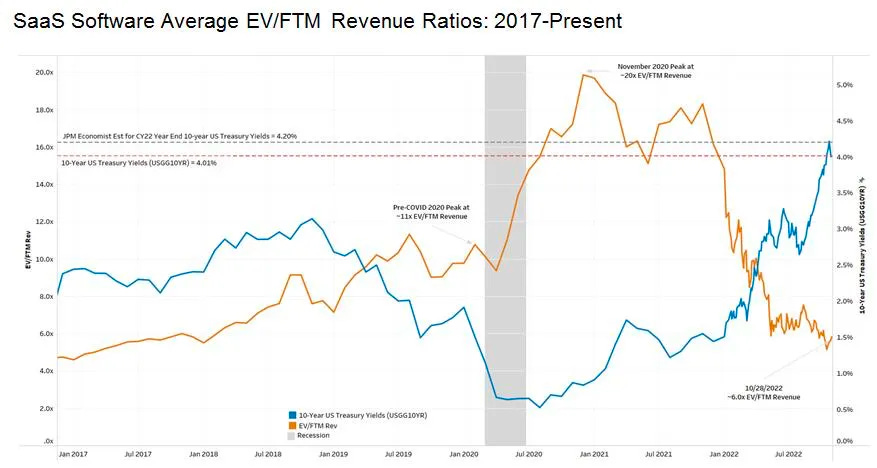

Interest rates determine how deeply you discount future cash flows, particularly for growth stage companies. When interest rates are higher, growth multiples compress and stock prices drop.

The higher interest rates stomped the bubble in public tech company multiples and pushed them back to in range with historical norms.

Multiples in the COVID era were the anomaly, not the 14 years prior. We are not going back to 2020-2021 valuation multiples (or anything close to it) until the next bubble.

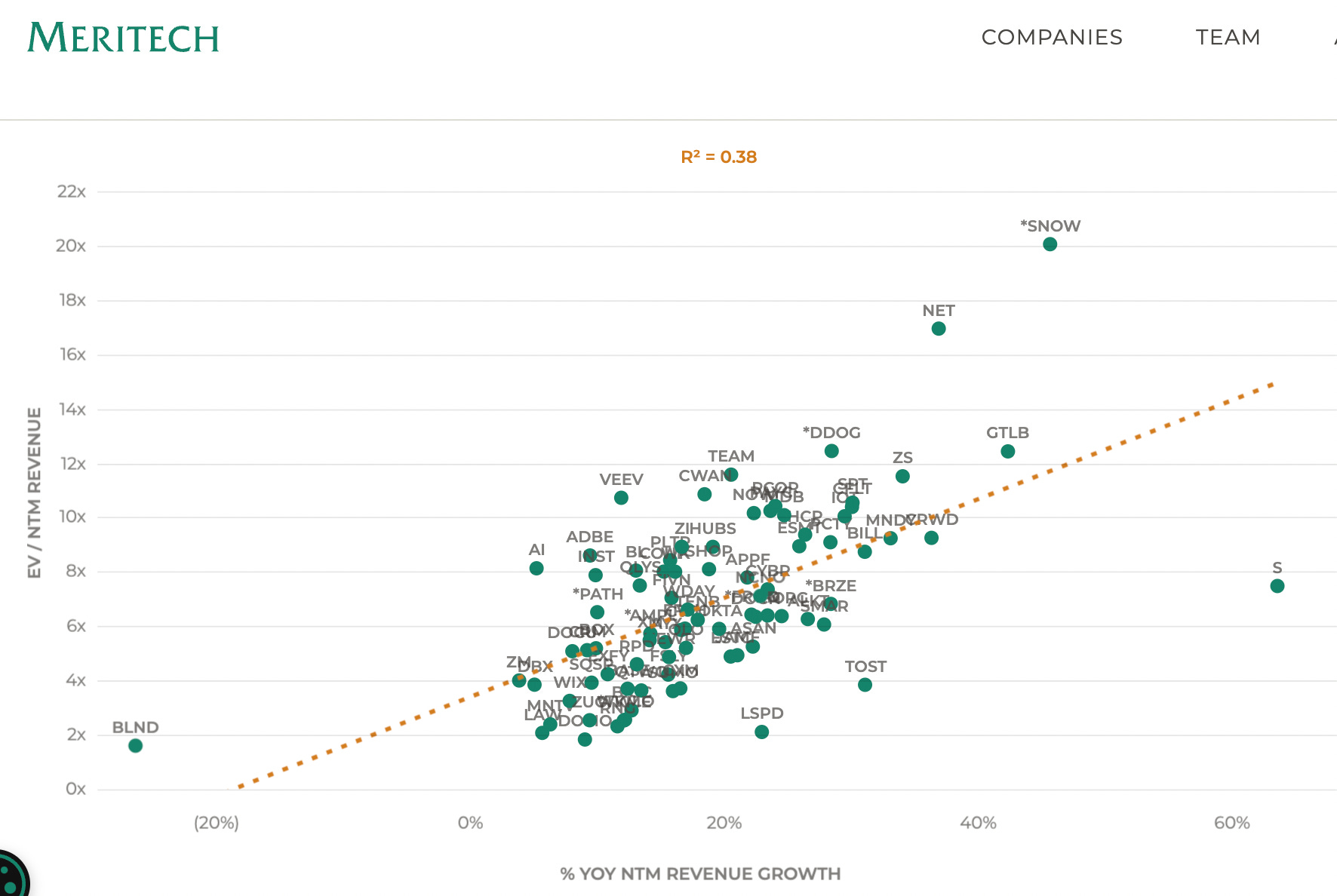

Every $1B in market cap = $100M to $150M in revenue growing 30% a year, $5B in market cap = $500M in forward revenue adding ~$150M in revenue a year (!)

Even if interest rates were to drop and SaaS multiples were to rise 50% they would be at roughly 10X forward revenue (up from 6X today). This means every $1B in market cap would need $100M or so of revenue (down from $150M today), growing 30% year over year. A $5B market cap would mean a company with $500M of revenue (down from $750M today) growing 30% year over year. So a company at that scale would need to be adding $150 million *per year* to be worth $5B. A $10B market cap is double that number ($1B in revenue adding $300M a year!). The current period is around historical norms, not an anomaly(!!).

Does a recession matter?

A recession at this point would slow down revenue growth for many companies[1]. This will drop NRR and new revenue and likely increase burn. Some tech startups that are on the margin from a survivability perspective will tip into a slow motion death as their growth slows. A recession would further drop public market expectations and multiples and that will bleed into later stage private rounds. Public market companies are already projecting slowing earnings and growth for 2023.

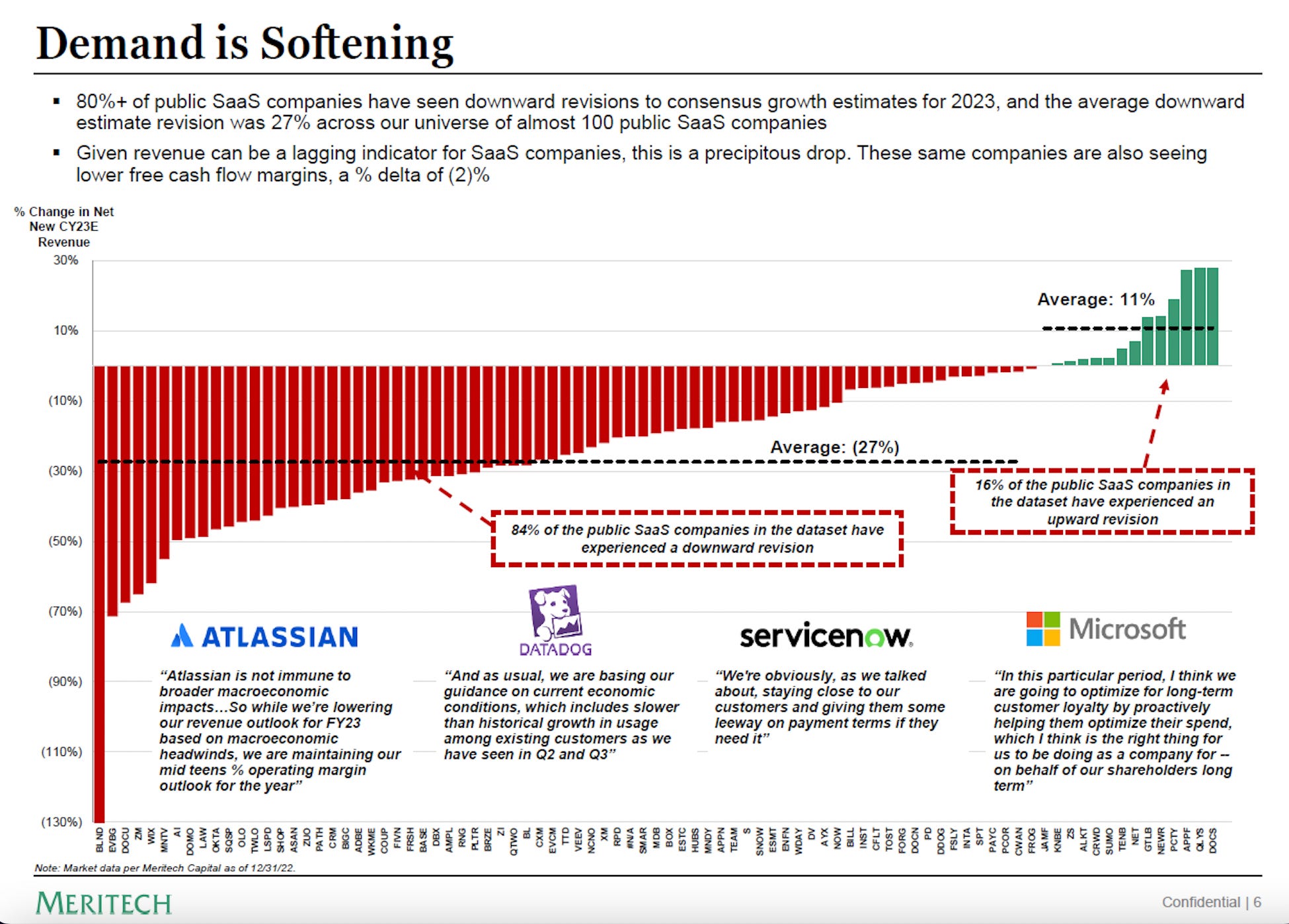

Irrespective of recession or not, software demand is softening (see chat below). Part of this is driven by overbuild and over purchase of software during the COVID era when both many “digital transformations” were undertaken, but also when capital was cheap and spending was not very ROI driven. With cost of capital going up and much corporate belt tightening, software spend is likely to continue to slow.

No matter, the valuation reset coming for private tech is so stark (50X to 100X ARR in 2021 → 10X) that a recession or drop in spend will only matter on the margin relative to the likely inability to raise money that is coming no matter what. Bloated, low-to-no product market fit companies, and ones that have product-market fit but overhired and overcapitalized will get stuck in different ways.

The macro economy and the startup valuation reset are now decoupling. The reset in private tech will happen roughly no matter what happens in the macro economy.

If your company has good underlying economics, can grow at a good rate, and is not dramatically overvalued, this could be a golden period for you as you soak up amazing talent and land great customers. If not…

There will be 3 types of outcomes –

1. Shut downs

More companies than people currently seem to think, will have no choice but to shut down. While some CEOs mention that “the worst case is a down round”, the reality is investors will look at money burned, progress by the company, and in many cases decide the state of the company and/or preference stack does not merit further investment. There is a large back log of companies that should have failed over the 4-5 years that kept going due to a loose capital environment. Things are going to catch up.

Now is a good time for CEOs to ask both insider investors, and new potential ones, what metrics they would want to see for them to be able to raise (note: these metric may be off in a year as investors are flooded by companies needing to fundraise, or dealing with their existing portfolio companies that will need tons of help).

Model it out – if you can get to profitability or “default alive” or “default fundable” that is great news.

If it looks like there are not many scenarios for a company to make it, now might be a good time to start an M&A process to sell the company, or to do an early shut down.

Your time is precious

Shutting down and giving up is really hard. Founders may have spent many years of their lives on a company that is not going to work. But rather than spend another 2 or 4 years waiting for the bank accounts to drain through multiple layoffs and venture debt draw downs it might be better to accept reality and throw in the towel.

For a founder (and their employees), those 2+ extra years may be amongst the potentially most productive years of their lives. The opportunity cost of not going to work on something better is too high. And to be able to do so without a cap table overhang, with a new team that fits a new product, may be a better way to proceed than continuing to grind on something that is not working or pivoting with the wrong team and cap table.

Investor incentives differ early vs late (and based on their role in VC firm)

Investors may or may not be aligned with a shutdown. Your early stage investors or those with a high performing fund may want you to keep going no matter what. While for them it is a free option, for you it is your life and livelihood! Early stage investors in particular may have used the latest round price of your company to raise a new fund (“look LPs-my investment track record is working!”) and may push back or dread a reset on valuation as it impacts their own ability to raise new venture funds. The personal incentives of the VC on your board within their firm may also impact things. For example, a VC may resist an otherwise rational low M&A exit or necessary down round in order to get promoted within their partnership or prove that things are working for them career-wise.

Other investors may prefer to get back 40 cents on the dollar, free up time, and also potentially free up founder and employee talent to back or work with again.

Think through your investors individual incentives as you consider what to do and hear (and filter) their opinion. A given company in a VC portfolio is part of a portfolio and may function as an option – while for you the company or how you otherwise spend your time is your entire livelihood. And never forget how precious your time is. Life is short, and productive years in which you can take a lot of risk are quite limited[2].

Anticipate 2nd, 3rd, and 4th rounds of layoffs as companies realize their business is not working, fundraising options are limited, and cash is running out. As mentioned above, doing a firesale or shutting down may be a better option in reality (and a harder pill to swallow short term) than a slow prolonged wind down.

Infinite runway companies

Some small subset of companies may also have roughly infinite cash but without a strong business. Maybe they raised $50M, $100M, or even $500M during good times but their business fundamentals are not there. A company that raised $500M and is burning $50M a year may have 10 years of runway but minimal revenue growth. Options in that case are to keep going, buying other companies to try to spark growth, selling to someone else for your cash, an ongoing search for something new (this roughly tends to never work for a late stage company), re-setting valuation (see below), or alternatively to shut down and return cash. A company that raised at 50X ARR will take 9 years growing 20% a year to grow to flat with its current valuation (assuming at 10X exit multiple).

During the 1990s internet bubble a few companies went public and then sat on $1B+ in cash, in some cases taking a decade to wind down. Just because you have infinite runway does not mean you should stick with it infinitely – your life and time are more precious.

2. M&A

Another path is to sell your company. As 2nd and 3rd rounds of layoffs happen there may be fewer and fewer buyers in the market for talent or new assets. After all, if a late stage company just did a big layoff it may be less likely to acquire (non-AI) talent. However, later stage growing companies, or public companies with strategic needs, may be active buyers. The very biggest, healthiest buyers (Google, Meta, etc) will be stymied by