Afridigest provides ideas & analysis for startup founders, operators, and investors across Africa and beyond.

This article explores key trends and developments in the African tech space in February 2022.

If you’re new, welcome 🙌 — you’ll receive a weekly digest of what happened in the African tech ecosystem every Monday and you’ll generally (but not always) receive an original essay on Saturdays. For past essays and digests, visit the archive.

Subscribe here:

After a dazzling January debut that saw Africa-focused tech startups raise over $430M from roughly 60 announced deals, fundraising in February was similarly feverish. The shortest month of the year witnessed approximately 60 announced tech deals across the continent comprising ~$600M in disclosed funding, according to Afridigest’s weekly tracking and methodology.1

So far, Africa-focused startups are on pace to raise ~$6 billion in disclosed funding and over $7 billion in total funding this year — assuming disclosed funding stays at ~85% of total funding. (In 2021, according to VC firm Partech Partners, fully disclosed deals represented 85% of total funding.)

In terms of the number of deals, Nigeria led the way with 18 deals, ~31% of the total number of deals announced in February across the continent. But these Nigerian deals represented ~57% of the ~$600 million raised in the month, thanks largely to Flutterwave’s $250M Series D (the continent’s second mega-round of 2022) — it alone accounted for ~42% of February’s total disclosed funding.

Regional spotlight

February saw a return to fundraising dominance for the ‘Big Four’ countries (i.e., Nigeria, South Africa, Kenya, and Egypt). Whereas there was quite a bit of geographic diversity in January with the Big Four then accounting for just ~50% of the debut month’s disclosed funding and ~75% of its deal count, Big Four countries in February accounted for a whopping 95% of the disclosed funding raised and ~86% of the deals announced in the month.

Sector breakout

Sector-wise, fintech unsurprisingly led the way again, attracting 52% of the disclosed funding in the month (up significantly from January’s 29%), followed by software’s 16% thanks largely to chat commerce software provider Clickatell’s $91M Series C.

The top five sectors attracting funding in the month were fintech, software, e-commerce, healthtech, and mobility. And rounding out the top 10 were logistics, connectivity, crypto, proptech, and insurtech.

Trends and developments

While fintech overall continues to be ascendant, developments in February emphasized one broad theme in the sector:

-

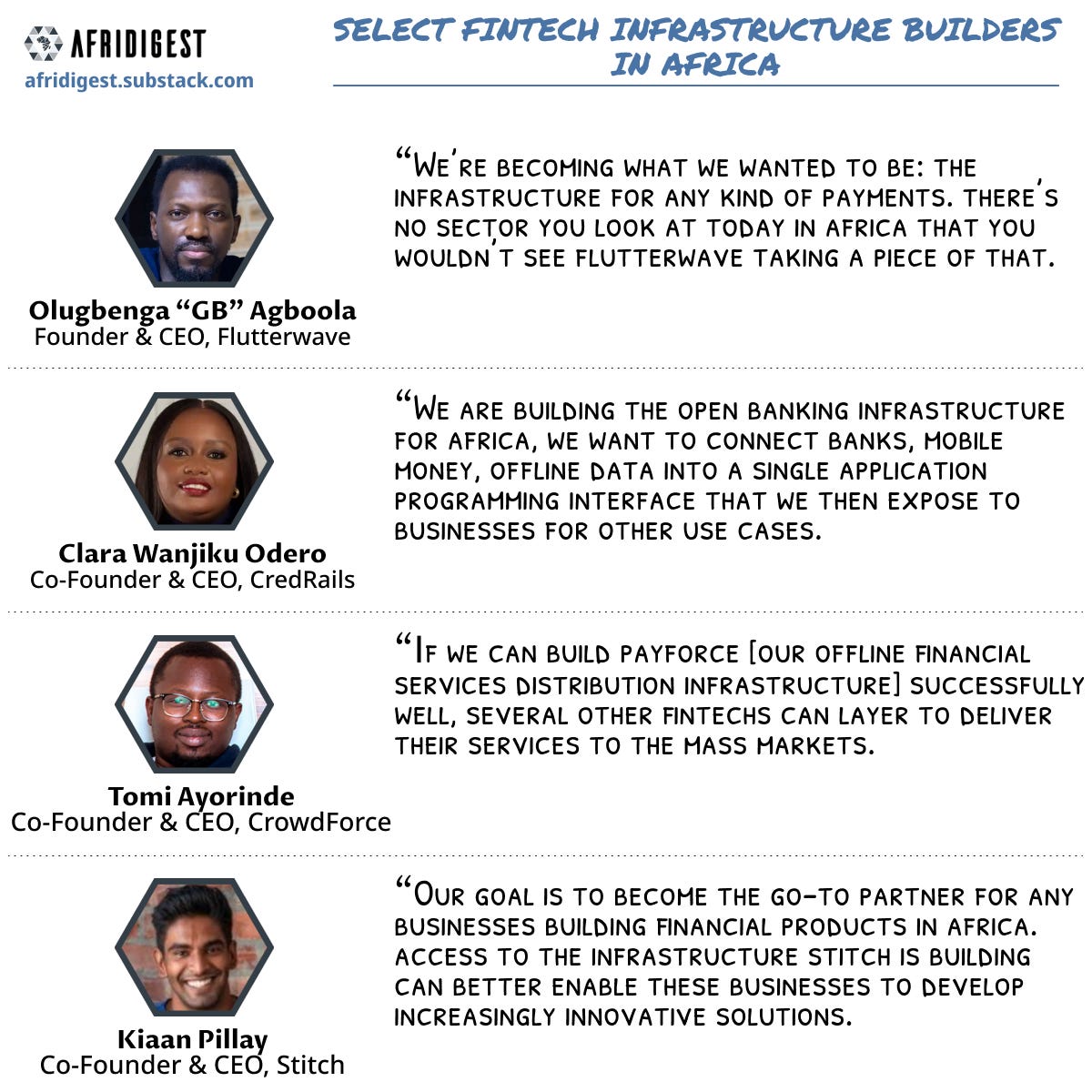

There’s still a massive opportunity in financial infrastructure. In 2020, I wrote in ‘The hierarchy of venture opportunities in emerging markets’ that “in an ecosystem, the prepotent layer is infrastructure … [and] there generally remain robust opportunities to create ventures that introduce basic or alternative infrastructure that can underpin the entire ecosystem.” This still rings true today, and February brought with it a strong reminder of the opportunity in building fintech infrastructure across the continent.

Nigeria’s Flutterwave is now the most valuable startup in Africa thanks largely to its initial focus on & success in building payments infrastructure; other payments infrastructure providers like Nigeria’s TeamApt and Kenya’s Ubawa raised rounds in the month; Egypt’s MoneyHash raised a pre-seed to build payments orchestration infrastructure that integrates and sits on top of payment providers like Flutterwave; South Africa’s Stitch and Kenya’s CredRails raised rounds to build open finance API infrastructure; and CrowdForce raised a round to grow its last-mile financial services distribution infrastructure.

While it’s hard not to lead with fintech given its dominance in February, perhaps it’s a well-worn theme for regular readers at this point. That said, February also saw interesting, fresh developments relative to strategic acquisitions and investments across the continent:

-

M&A in African tech is heating up. At the start of the year, I put forth that an increase in strategic bolt-on & tuck-in acquisitions is among five major trends to expect across Africa’s startup ecosystem in 2022. And thanks to a very acquisitive February, this seems prescient given the uptick during the first two months of the year, with at least eight acquisitions announced in February alone. (And this trend continues into March with an additional three acquisitions already announced so far, just days into the new month.)

-

Strategic minority investments are on the rise. Coupled with the upsurge in outright and majority acquisitions, February also saw an increasing number of companies take strategic minority positions in various startups (in Egypt mostly, but elsewhere too).

Egyptian non-bank consumer finance provider Contact Financial invested $9M in Egyptian shopping browser Wasla to help it deploy BNPL offerings, Egypt’s Brimore invested $5M in its logistics spinoff Milezmore, the UAE’s super app (& Uber subsidiary) Careem took a stake in Egyptian food delivery platform Elmenus to gain more exposure to a strategic vertical in a high-potential market, and Mauritian survey-focused gig economy platform Rwazi invested in Mauritian HR tech platform KrediblePro which helps it source talent.

Switching gears and looking back to the article, ‘Key trends & themes to look for across Africa in 2022,’ I offered there that “2022 could see the rise of crypto/blockchain/web3 projects deployed across the African continent as it increasingly becomes the global center of utility-driven ‘web3.’” And February brought good tidings for web3 in Africa:

-

The race to onboard African users to web3 is on. In early February, Nigeria’s Nestcoin, a builder, operator, and investor in web3 applications (in the mold of the US’s Digital Cur